Small Registered AIFMs, Big Regulatory Shift

In the next few weeks, we are expecting draft rules setting out the new regulatory framework for managers in the UK. The proposals follow an FCA Call for Input and HMT Consultation published back in April 2025. Since then, much of the attention has been focused on the impact on existing FCA authorised managers. However, the brunt of the new rules will likely be felt by a smaller sub-set of managers who have, until now, operated under a far lighter touch regulatory regime.The current regime

The Small Registered AIFM regime allows certain managers an exemption to the full requirements of the Alternative Investment Fund Managers Directive (AIFMD). These firms only need to register with FCA rather than needing to be authorised. This option is available to the following managers providing assets managed remain under the 500m EUR threshold:1. Property fund managers;2. Internally managed, listed closed-ended investment companies (LCICs, such as investment trusts); or3. Managers of Social Entrepreneurship Funds (SEF) and Venture Capital Funds (RVECA).LCICs operate within a comprehensive regulatory framework; they are subject to the UK Listing Rules (UKLRs), Disclosure Guidance and Transparency Rules, the Prospectus Regulation Rules and the UK Market Abuse Regime. RVECA managers are similarly subject to additional requirements (albeit to a lesser extent) due to the requirements set out in the RVECA Regulation.Property fund managers, however, operate in a very light regulatory environment. Only very basic requirements under AIFMD apply, including: requirements relating to the disciplinary history of the directors, restrictions to the type of assets invested in (land) and light-touch FCA reporting and AuM monitoring and notification requirements.FCA and UK Government have identified several identified issues with the regime as a result, including:The current regime could create a ‘halo effect’ where consumers assume the firms are subject to FCA control and oversight because they are registered.The regime thresholds create cliff-edge risks, whereby a sub-threshold firm is subject to minimal requirements but, once their AuM exceeds the threshold, there is a significant increase in requirements.Some firms are taking advantage of the Small Registered Regime exemption by specifically structuring their funds to qualify for the exemption, benefiting from the ‘Halo Effect’ while avoiding strict oversight

Upcoming changes

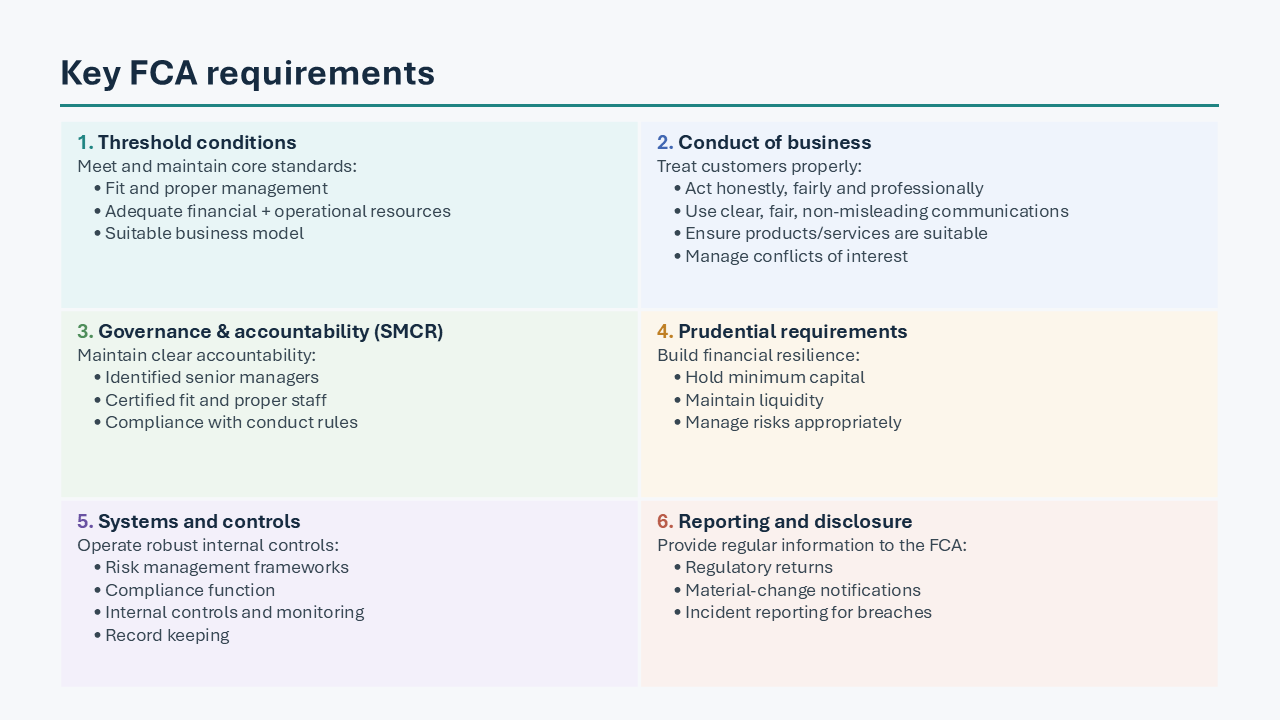

Under the new framework, firms currently in the registered regime (excluding SEF/RVECA managers, who will be addressed separately) will be required to seek full FCA authorisation. If authorisation is granted, these firms will need to transition into a new tiered system where they would be subject to "core baseline standards”. Applying for FCA authorisation and thereafter complying with FCA rules are significant undertakings. The exact requirements that will apply are not yet finalised but we expect it will largely mirror existing requirements for small authorised managers, summarised here:

Transitioning from a registered to an authorised firm is a significant task. This process will involve up-front costs and increased operational and administrative burdens. Firms should engage with the topic now to ensure they are fully prepared for the additional requirements. How can ComplyCraft help

We work with all types of managers. We have in‑depth expertise across alternatives, private equity, venture capital firms (including EIS managers), and property and infrastructure fund managers. Our team has successfully completed hundreds of applications (both as consultants and while working at the FCA) giving us a unique understanding of what the regulator expects in practice.Our services are flexible: we can “hold the pen” and manage the entire process for you, or provide targeted advice and independent review to support your internal team. Either way, we take a pragmatic, hands‑on approach to help you navigate the authorisation process efficiently and with confidence. Once authorised, our team of experienced consultants can support you with ongoing compliance needs such as implementing processes and procedures to comply with FCA requirements. Please reach if you’d like to discuss what these developments mean for you.